It was the first International Day of Family Remittances last month. The day was commemorated during a UN-led forum on remittances and development that aims to ratchet up efforts to reduce the cost of sending money between countries for both the 250 million migrants working abroad and the 750 million people back home who depend on these funds.

International organisations have been trying to reduce the fees charged for sending money for several years. In 2009, the G8 group of leading economies adopted the 5x5 Objective to reduce the average charges from ten to five per cent of the amount sent, and to do this within five years (that is, by 2014). Other intergovernmental organisations, including the G20, swiftly endorsed this goal.

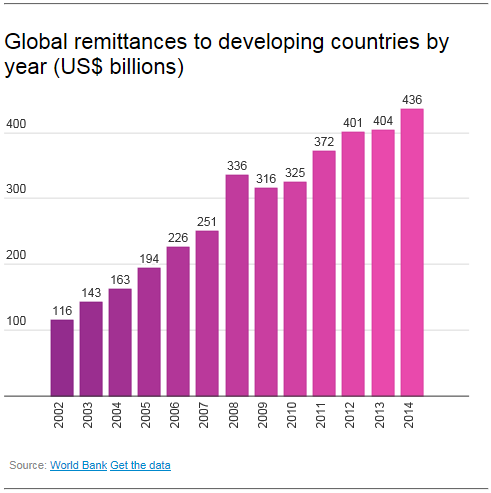

The potential impact is not to be sniffed at. Remittances to developing countries are estimated to have reached US$436 billion in 2014, an increase of 7.8 per cent from 2013. This means that reducing the cost of sending money by just a few percentage points would save billions of dollars a year for migrants and their families.

So did the world hit the 5x5 target? The latest data suggests that the average total fees charged for sending money was 7.7 per cent during the second quarter of 2015 — a decline of around two percentage points since 2009, but less than the five per cent objective. [1] Charges are also lower in some transaction routes than others, with prices fluctuating depending on the number of migrants and service providers in a certain country. [2] For example, in South Asia the average cost of sending money is now 5.7 per cent, while in Sub-Saharan Africa it is 9.7 per cent.

But there are reasons to hope prices will continue to tumble. One major factor shaking up the global market and spurring competition is the growth of online transfer companies, particularly those using mobile money systems. The World Bank estimates that the average cost of sending money using online products is 5.48 per cent of the amount sent — almost in line with the 5x5 objective. [1]

One successful online service is WorldRemit, a relatively new player in the sector. Last month, the firm won an award for best practice at the Global Forum on Remittances and Development 2015 Awards for its innovative use of mobile technology.

Central to its business model are online transfers to ‘mobile money’ accounts. This is a particular advantage in poor regions where most people lack bank accounts, but have access to mobile phones, and use their phone accounts for everyday payments. For example, a migrant worker can use a smartphone app to send money to family members, the money goes directly into their family’s mobile account, and they can then use this to make payments without needing to collect the money in cash from an agent.

Greater transparency about the actual cost of sending money and more information about price differences between companies and products are also helping to slash costs. For example, the World Bank’s Remittance Prices Worldwide portal, launched in 2008, monitors the cost of sending money, so that users can compare prices across companies and get clear information on remittance charges. Combined, these measures signal hope for a further drop in fees for the millions of migrants who send and receive money.

This blog was first published on SciDevNet.

References

[1] Remittance prices worldwide (World Bank, June 2015)

[2] Thorsten Beck and María Soledad Martínez Pería What explains the price of remittances? An examination across 119 country corridors (The World Bank Economic Review, 23 May 2011)